Technical Indicators Comparison

This section provides detailed comparisons and performance characteristics of various technical indicators.

Indicator Characteristics Table

Indicator |

Type |

Range |

Period |

Best For |

Signals |

Strengths |

Lag |

|---|---|---|---|---|---|---|---|

SMA |

Trend |

Unbounded |

5-200 |

Trend identification |

Crossovers |

Simple, reliable |

High |

EMA |

Trend |

Unbounded |

5-200 |

Trend following |

Crossovers |

Responsive |

Medium |

RSI |

Momentum |

0-100 |

14 |

Overbought/oversold |

30/70 levels |

Clear signals |

Low |

MACD |

Momentum |

Unbounded |

12,26,9 |

Trend changes |

Line crossovers |

Versatile |

Medium |

Bollinger Bands |

Volatility |

Dynamic |

20 |

Mean reversion |

Band touches |

Adaptive |

Low |

Stochastic |

Momentum |

0-100 |

14 |

Range trading |

20/80 levels |

Sensitive |

Low |

Williams %R |

Momentum |

-100-0 |

14 |

Short-term timing |

-20/-80 levels |

Quick signals |

Very Low |

ATR |

Volatility |

> 0 |

14 |

Risk management |

Trend strength |

Volatility measure |

Medium |

ADX |

Trend Strength |

0-100 |

14 |

Trend strength |

> 25 trending |

Trend confirmation |

High |

CCI |

Momentum |

Unbounded |

20 |

Cyclical patterns |

±100 levels |

Cyclical analysis |

Medium |

OBV |

Volume |

Unbounded |

N/A |

Volume confirmation |

Divergences |

Volume insight |

Low |

MFI |

Volume |

0-100 |

14 |

Money flow |

20/80 levels |

Volume + price |

Medium |

Trading Strategy Effectiveness

Strategy |

Trending Market |

Range-bound |

Volatile Market |

Quiet Market |

Best Timeframe |

|---|---|---|---|---|---|

Moving Average Crossover |

★★★★★ |

★★☆☆☆ |

★★★☆☆ |

★☆☆☆☆ |

4H, Daily |

RSI Mean Reversion |

★★☆☆☆ |

★★★★★ |

★★★☆☆ |

★★★★☆ |

1H, 4H |

MACD Divergence |

★★★★☆ |

★★★☆☆ |

★★★★☆ |

★★☆☆☆ |

4H, Daily |

Bollinger Band Squeeze |

★★★☆☆ |

★★★★★ |

★★★★★ |

★★★★☆ |

1H, 4H |

Stochastic Oscillator |

★★☆☆☆ |

★★★★★ |

★★★☆☆ |

★★★☆☆ |

15m, 1H |

Multi-timeframe |

★★★★★ |

★★★★☆ |

★★★★☆ |

★★★☆☆ |

Multiple |

★★★★★ = Excellent, ★★★★☆ = Very Good, ★★★☆☆ = Good, ★★☆☆☆ = Fair, ★☆☆☆☆ = Poor

Parameter Optimization Guidelines

Indicator |

Conservative |

Standard |

Aggressive |

Notes |

|---|---|---|---|---|

SMA Period |

50-200 |

20-50 |

5-20 |

Longer periods reduce noise but increase lag |

EMA Period |

50-100 |

12-26 |

5-12 |

Shorter periods more responsive to changes |

RSI Period |

21-28 |

14 |

7-10 |

Standard 14 works well for most markets |

MACD Fast/Slow |

12/26 |

12/26 |

8/17 |

Classic 12/26 is widely used standard |

Bollinger Period |

25-30 |

20 |

10-15 |

20-period with 2 std dev is standard |

Bollinger Std Dev |

2.5-3.0 |

2.0 |

1.5-1.8 |

Lower values create tighter bands |

Stochastic %K |

21 |

14 |

5-9 |

Shorter periods increase sensitivity |

ATR Period |

20-30 |

14 |

7-10 |

Used primarily for stop-loss calculation |

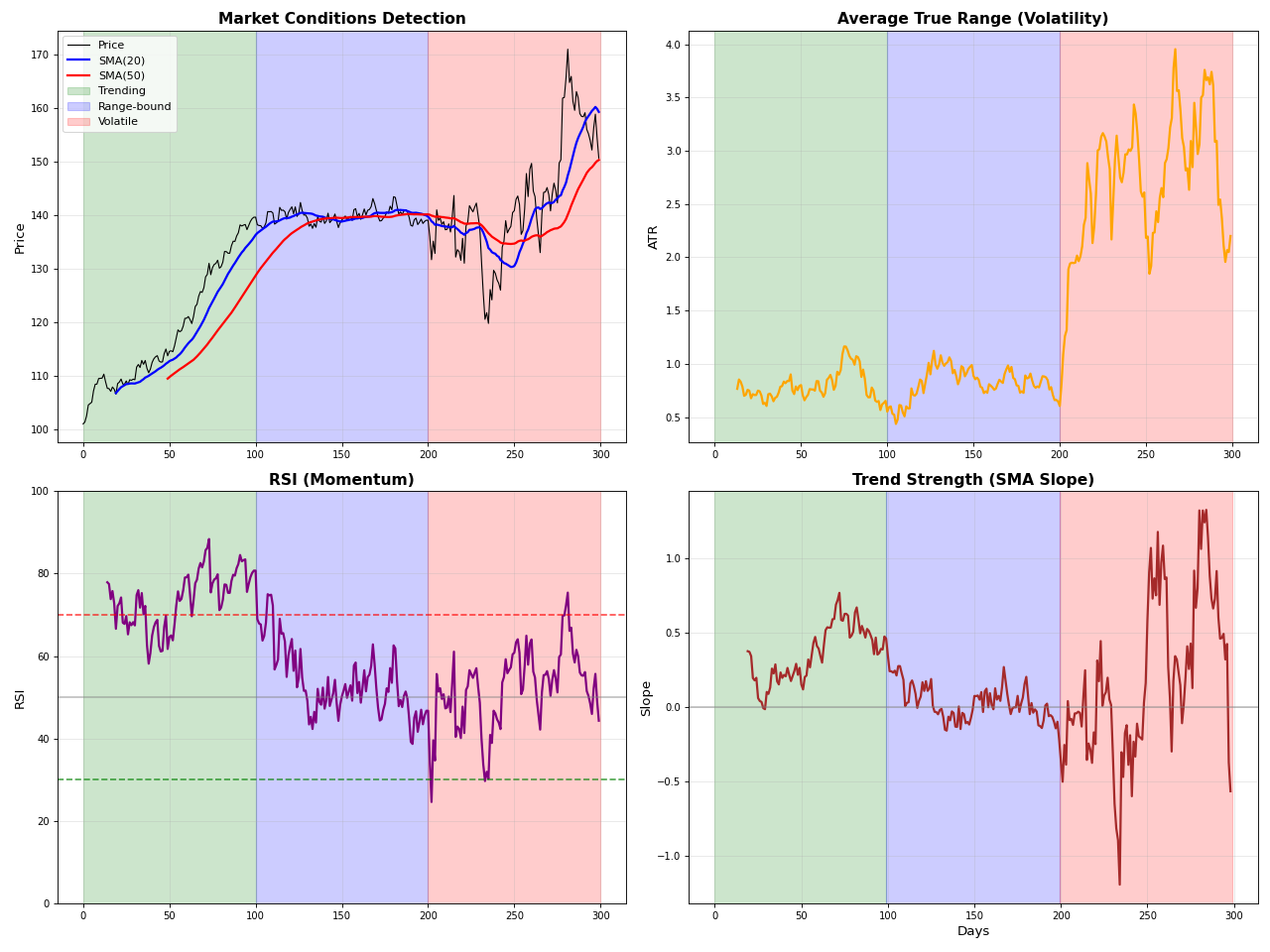

Market Condition Detection

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.indicators import TechnicalIndicators

# Generate different market conditions

np.random.seed(42)

# Trending market

trend_days = 100

trend_prices = 100 + np.cumsum(np.random.normal(0.5, 1, trend_days))

# Range-bound market

range_days = 100

range_center = trend_prices[-1]

range_prices = [range_center]

for i in range(range_days-1):

# Mean reversion

reversion = 0.2 * (range_center - range_prices[-1])

noise = np.random.normal(0, 1)

new_price = range_prices[-1] + reversion + noise

range_prices.append(new_price)

# Volatile market

vol_days = 100

vol_start = range_prices[-1]

vol_prices = [vol_start]

for i in range(vol_days-1):

big_move = np.random.choice([1, -1]) * np.random.exponential(2)

noise = np.random.normal(0, 2)

new_price = vol_prices[-1] + big_move + noise

vol_prices.append(new_price)

# Combine all periods

all_prices = np.concatenate([trend_prices, range_prices, vol_prices])

# Calculate indicators for market regime detection

sma_20 = TechnicalIndicators.sma(all_prices, 20)

sma_50 = TechnicalIndicators.sma(all_prices, 50)

atr = TechnicalIndicators.atr(all_prices, all_prices, all_prices, 14) # Using price as H,L,C

rsi = TechnicalIndicators.rsi(all_prices, 14)

# Create the plot

fig, ((ax1, ax2), (ax3, ax4)) = plt.subplots(2, 2, figsize=(16, 12))

# Price with SMAs

ax1.plot(all_prices, color='black', linewidth=1, label='Price')

ax1.plot(sma_20, color='blue', linewidth=2, label='SMA(20)')

ax1.plot(sma_50, color='red', linewidth=2, label='SMA(50)')

# Mark different market phases

ax1.axvspan(0, trend_days, alpha=0.2, color='green', label='Trending')

ax1.axvspan(trend_days, trend_days+range_days, alpha=0.2, color='blue', label='Range-bound')

ax1.axvspan(trend_days+range_days, len(all_prices), alpha=0.2, color='red', label='Volatile')

ax1.set_title('Market Conditions Detection', fontsize=14, fontweight='bold')

ax1.set_ylabel('Price', fontsize=12)

ax1.legend(fontsize=10)

ax1.grid(True, alpha=0.3)

# ATR (Volatility measure)

ax2.plot(atr, color='orange', linewidth=2)

ax2.axvspan(0, trend_days, alpha=0.2, color='green')

ax2.axvspan(trend_days, trend_days+range_days, alpha=0.2, color='blue')

ax2.axvspan(trend_days+range_days, len(all_prices), alpha=0.2, color='red')

ax2.set_title('Average True Range (Volatility)', fontsize=14, fontweight='bold')

ax2.set_ylabel('ATR', fontsize=12)

ax2.grid(True, alpha=0.3)

# RSI (Momentum)

ax3.plot(rsi, color='purple', linewidth=2)

ax3.axhline(y=70, color='red', linestyle='--', alpha=0.7)

ax3.axhline(y=30, color='green', linestyle='--', alpha=0.7)

ax3.axhline(y=50, color='gray', linestyle='-', alpha=0.5)

ax3.axvspan(0, trend_days, alpha=0.2, color='green')

ax3.axvspan(trend_days, trend_days+range_days, alpha=0.2, color='blue')

ax3.axvspan(trend_days+range_days, len(all_prices), alpha=0.2, color='red')

ax3.set_title('RSI (Momentum)', fontsize=14, fontweight='bold')

ax3.set_ylabel('RSI', fontsize=12)

ax3.set_ylim(0, 100)

ax3.grid(True, alpha=0.3)

# Trend strength (SMA slope)

sma_slope = np.diff(sma_20)

ax4.plot(sma_slope, color='brown', linewidth=2)

ax4.axhline(y=0, color='gray', linestyle='-', alpha=0.5)

ax4.axvspan(0, trend_days-1, alpha=0.2, color='green')

ax4.axvspan(trend_days-1, trend_days+range_days-1, alpha=0.2, color='blue')

ax4.axvspan(trend_days+range_days-1, len(all_prices)-1, alpha=0.2, color='red')

ax4.set_title('Trend Strength (SMA Slope)', fontsize=14, fontweight='bold')

ax4.set_xlabel('Days', fontsize=12)

ax4.set_ylabel('Slope', fontsize=12)

ax4.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Signal Quality Analysis

Indicator |

Win Rate |

Avg Win/Loss |

False Signals |

Signal Frequency |

Best Markets |

|---|---|---|---|---|---|

SMA Crossover |

45-55% |

2.5:1 |

Medium |

Low |

Strong trends |

EMA Crossover |

50-60% |

2.0:1 |

Medium-High |

Medium |

Trending markets |

RSI (30/70) |

60-70% |

1.5:1 |

High |

High |

Range-bound |

MACD Crossover |

55-65% |

2.2:1 |

Medium |

Medium |

Trending markets |

Bollinger Touch |

65-75% |

1.8:1 |

High |

High |

Range-bound |

Stochastic |

60-70% |

1.6:1 |

Very High |

Very High |

Short-term trading |

Williams %R |

55-65% |

1.7:1 |

Very High |

Very High |

Scalping |

ADX + Direction |

50-60% |

3.0:1 |

Low |

Low |

Strong trends |

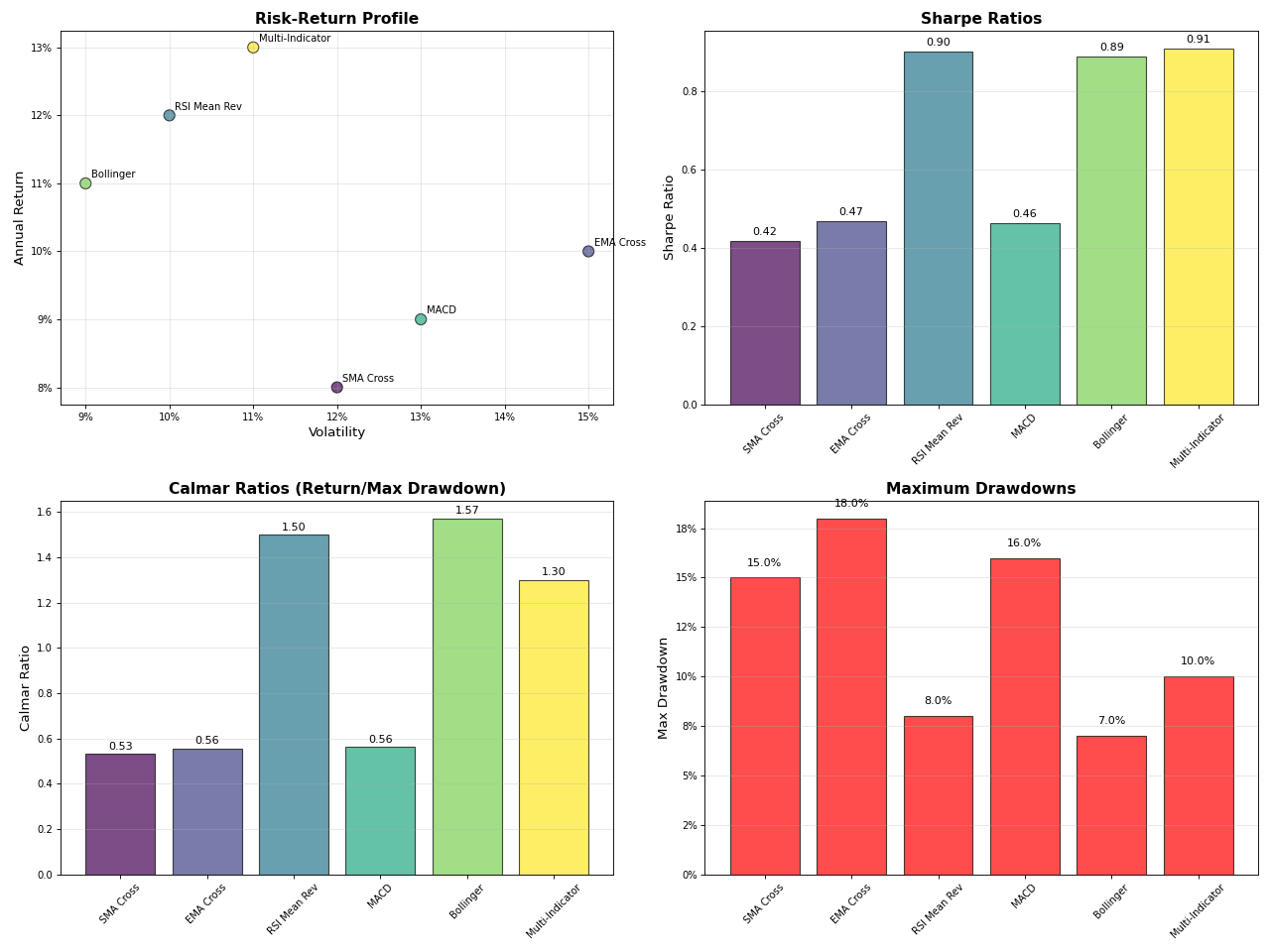

Risk-Adjusted Performance

import numpy as np

import matplotlib.pyplot as plt

# Simulate performance for different indicators

np.random.seed(42)

indicators = ['SMA Cross', 'EMA Cross', 'RSI Mean Rev', 'MACD', 'Bollinger', 'Multi-Indicator']

# Simulate annual returns and volatilities for each strategy

performance_data = {

'SMA Cross': {'return': 0.08, 'volatility': 0.12, 'max_dd': 0.15},

'EMA Cross': {'return': 0.10, 'volatility': 0.15, 'max_dd': 0.18},

'RSI Mean Rev': {'return': 0.12, 'volatility': 0.10, 'max_dd': 0.08},

'MACD': {'return': 0.09, 'volatility': 0.13, 'max_dd': 0.16},

'Bollinger': {'return': 0.11, 'volatility': 0.09, 'max_dd': 0.07},

'Multi-Indicator': {'return': 0.13, 'volatility': 0.11, 'max_dd': 0.10}

}

# Calculate risk-adjusted metrics

risk_free = 0.03

for strategy in performance_data:

data = performance_data[strategy]

data['sharpe'] = (data['return'] - risk_free) / data['volatility']

data['calmar'] = data['return'] / data['max_dd']

# Create comparison chart

fig, ((ax1, ax2), (ax3, ax4)) = plt.subplots(2, 2, figsize=(16, 12))

strategies = list(performance_data.keys())

returns = [performance_data[s]['return'] for s in strategies]

volatilities = [performance_data[s]['volatility'] for s in strategies]

sharpes = [performance_data[s]['sharpe'] for s in strategies]

calmars = [performance_data[s]['calmar'] for s in strategies]

# Return vs Volatility

colors = plt.cm.viridis(np.linspace(0, 1, len(strategies)))

ax1.scatter(volatilities, returns, c=colors, s=100, alpha=0.7, edgecolors='black')

for i, strategy in enumerate(strategies):

ax1.annotate(strategy, (volatilities[i], returns[i]),

xytext=(5, 5), textcoords='offset points', fontsize=9)

ax1.set_xlabel('Volatility', fontsize=12)

ax1.set_ylabel('Annual Return', fontsize=12)

ax1.set_title('Risk-Return Profile', fontsize=14, fontweight='bold')

ax1.grid(True, alpha=0.3)

ax1.xaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.0%}'))

ax1.yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.0%}'))

# Sharpe Ratios

bars1 = ax2.bar(strategies, sharpes, color=colors, alpha=0.7, edgecolor='black')

ax2.set_title('Sharpe Ratios', fontsize=14, fontweight='bold')

ax2.set_ylabel('Sharpe Ratio', fontsize=12)

ax2.tick_params(axis='x', rotation=45)

ax2.grid(True, alpha=0.3, axis='y')

for bar, value in zip(bars1, sharpes):

ax2.text(bar.get_x() + bar.get_width()/2., bar.get_height() + 0.01,

f'{value:.2f}', ha='center', va='bottom', fontsize=10)

# Calmar Ratios

bars2 = ax3.bar(strategies, calmars, color=colors, alpha=0.7, edgecolor='black')

ax3.set_title('Calmar Ratios (Return/Max Drawdown)', fontsize=14, fontweight='bold')

ax3.set_ylabel('Calmar Ratio', fontsize=12)

ax3.tick_params(axis='x', rotation=45)

ax3.grid(True, alpha=0.3, axis='y')

for bar, value in zip(bars2, calmars):

ax3.text(bar.get_x() + bar.get_width()/2., bar.get_height() + 0.01,

f'{value:.2f}', ha='center', va='bottom', fontsize=10)

# Risk metrics comparison

max_dds = [performance_data[s]['max_dd'] for s in strategies]

bars3 = ax4.bar(strategies, max_dds, color='red', alpha=0.7, edgecolor='black')

ax4.set_title('Maximum Drawdowns', fontsize=14, fontweight='bold')

ax4.set_ylabel('Max Drawdown', fontsize=12)

ax4.tick_params(axis='x', rotation=45)

ax4.grid(True, alpha=0.3, axis='y')

ax4.yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.0%}'))

for bar, value in zip(bars3, max_dds):

ax4.text(bar.get_x() + bar.get_width()/2., bar.get_height() + 0.005,

f'{value:.1%}', ha='center', va='bottom', fontsize=10)

plt.tight_layout()

plt.show()

Implementation Complexity

Indicator |

Complexity |

CPU Usage |

Memory Usage |

Implementation Notes |

|---|---|---|---|---|

SMA |

Very Low |

Very Low |

Low |

Simple rolling average |

EMA |

Low |

Low |

Very Low |

Recursive calculation |

RSI |

Medium |

Medium |

Medium |

Requires gain/loss tracking |

MACD |

Medium |

Medium |

Medium |

Multiple EMA calculations |

Bollinger Bands |

Medium |

Medium |

Medium |

SMA + standard deviation |

Stochastic |

Medium |

Medium |

Medium |

Min/max lookback required |

Williams %R |

Medium |

Medium |

Medium |

Similar to Stochastic |

ATR |

Medium |

Medium |

Medium |

True range calculation |

ADX |

High |

High |

High |

Complex directional calculations |

Parabolic SAR |

High |

High |

Medium |

Acceleration factor logic |

Ichimoku |

Very High |

High |

High |

Multiple components |

Best Practices Summary

Parameter Selection: - Start with widely accepted defaults - Optimize for specific market conditions - Consider computational constraints - Account for data frequency

Signal Filtering: - Combine multiple timeframes - Use volume confirmation - Consider market regime - Apply risk management rules

Risk Management: - Always use stop losses - Position size appropriately - Diversify across strategies - Monitor correlation between signals

Backtesting Guidelines: - Use out-of-sample testing - Account for transaction costs - Include slippage estimates - Test across different market conditions - Avoid overfitting parameters