Visual Guide

This section provides comprehensive visual representations, charts, and tables for portfolio-lib indicators and analytics.

Technical Indicators Visualization

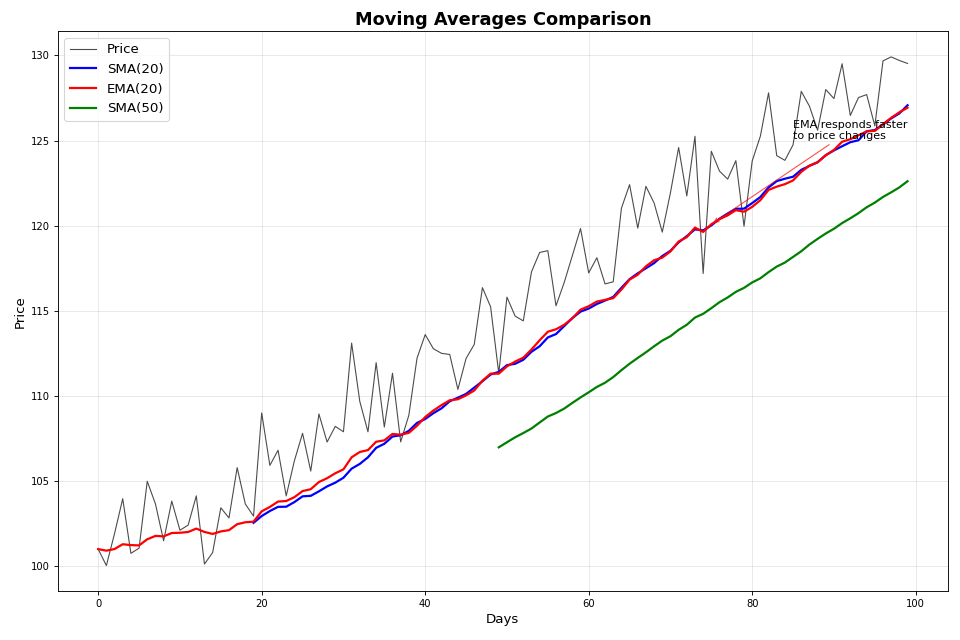

Moving Averages Comparison

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.indicators import TechnicalIndicators

# Generate sample price data

np.random.seed(42)

days = 100

trend = np.linspace(100, 130, days)

noise = np.random.normal(0, 2, days)

prices = trend + noise

# Calculate different moving averages

sma_20 = TechnicalIndicators.sma(prices, 20)

ema_20 = TechnicalIndicators.ema(prices, 20)

sma_50 = TechnicalIndicators.sma(prices, 50)

# Create the plot

fig, ax = plt.subplots(figsize=(12, 8))

# Plot price and moving averages

ax.plot(prices, label='Price', linewidth=1, alpha=0.7, color='black')

ax.plot(sma_20, label='SMA(20)', linewidth=2, color='blue')

ax.plot(ema_20, label='EMA(20)', linewidth=2, color='red')

ax.plot(sma_50, label='SMA(50)', linewidth=2, color='green')

# Styling

ax.set_title('Moving Averages Comparison', fontsize=16, fontweight='bold')

ax.set_xlabel('Days', fontsize=12)

ax.set_ylabel('Price', fontsize=12)

ax.legend(fontsize=12)

ax.grid(True, alpha=0.3)

# Add annotations

ax.annotate('EMA responds faster\nto price changes',

xy=(75, ema_20[75]), xytext=(85, ema_20[75] + 5),

arrowprops=dict(arrowstyle='->', color='red', alpha=0.7),

fontsize=10, ha='left')

plt.tight_layout()

plt.show()

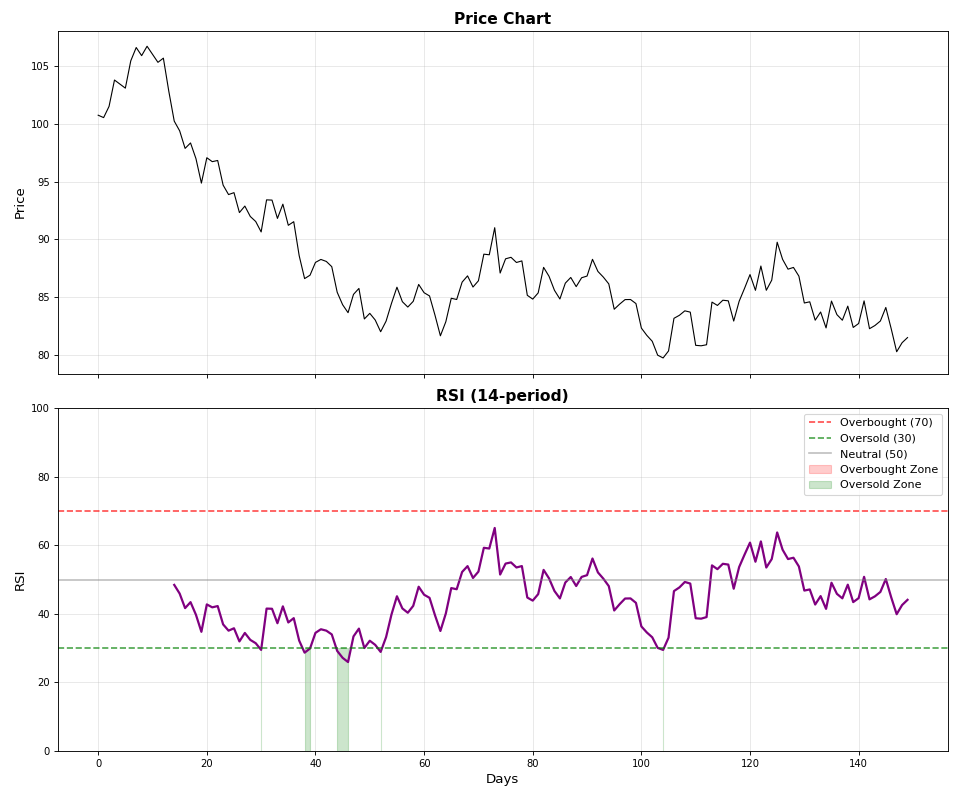

RSI Overbought/Oversold Analysis

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.indicators import TechnicalIndicators

# Generate volatile price data

np.random.seed(42)

prices = 100 + np.cumsum(np.random.randn(150) * 1.5)

rsi = TechnicalIndicators.rsi(prices, 14)

# Create subplots

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(12, 10), sharex=True)

# Price chart

ax1.plot(prices, color='black', linewidth=1)

ax1.set_title('Price Chart', fontsize=14, fontweight='bold')

ax1.set_ylabel('Price', fontsize=12)

ax1.grid(True, alpha=0.3)

# RSI chart

ax2.plot(rsi, color='purple', linewidth=2)

ax2.axhline(y=70, color='red', linestyle='--', alpha=0.7, label='Overbought (70)')

ax2.axhline(y=30, color='green', linestyle='--', alpha=0.7, label='Oversold (30)')

ax2.axhline(y=50, color='gray', linestyle='-', alpha=0.5, label='Neutral (50)')

# Fill overbought/oversold areas

ax2.fill_between(range(len(rsi)), 70, 100, where=(rsi >= 70), alpha=0.2, color='red', label='Overbought Zone')

ax2.fill_between(range(len(rsi)), 0, 30, where=(rsi <= 30), alpha=0.2, color='green', label='Oversold Zone')

ax2.set_title('RSI (14-period)', fontsize=14, fontweight='bold')

ax2.set_xlabel('Days', fontsize=12)

ax2.set_ylabel('RSI', fontsize=12)

ax2.set_ylim(0, 100)

ax2.legend(fontsize=10)

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

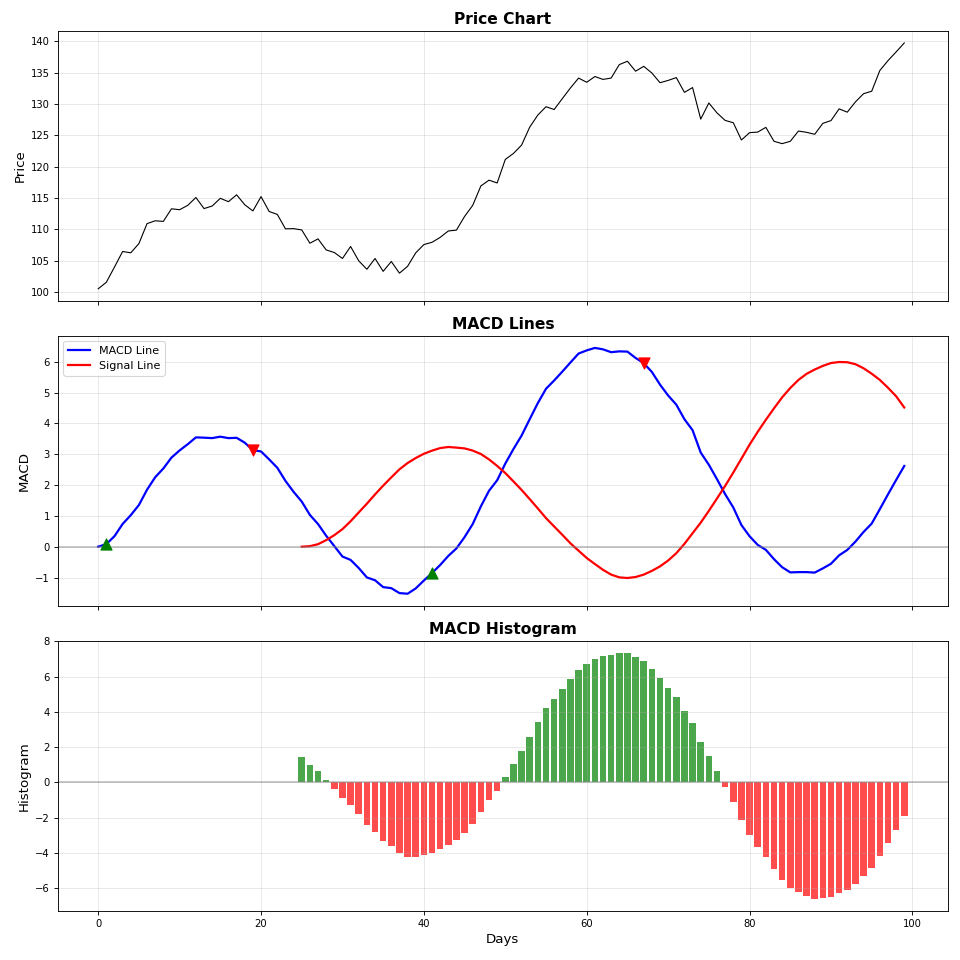

MACD Signal Analysis

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.indicators import TechnicalIndicators

# Generate trending price data

np.random.seed(42)

base_trend = np.linspace(100, 140, 100)

cycle = 10 * np.sin(np.linspace(0, 4*np.pi, 100))

noise = np.random.normal(0, 1, 100)

prices = base_trend + cycle + noise

# Calculate MACD

macd_line, signal_line, histogram = TechnicalIndicators.macd(prices)

# Create subplots

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(12, 12), sharex=True)

# Price chart

ax1.plot(prices, color='black', linewidth=1)

ax1.set_title('Price Chart', fontsize=14, fontweight='bold')

ax1.set_ylabel('Price', fontsize=12)

ax1.grid(True, alpha=0.3)

# MACD Lines

ax2.plot(macd_line, color='blue', linewidth=2, label='MACD Line')

ax2.plot(signal_line, color='red', linewidth=2, label='Signal Line')

ax2.axhline(y=0, color='gray', linestyle='-', alpha=0.5)

# Highlight crossovers

macd_clean = macd_line[~np.isnan(macd_line)]

signal_clean = signal_line[~np.isnan(signal_line)]

min_len = min(len(macd_clean), len(signal_clean))

if min_len > 1:

for i in range(1, min_len):

if macd_clean[i] > signal_clean[i] and macd_clean[i-1] <= signal_clean[i-1]:

ax2.scatter(i, macd_clean[i], color='green', s=100, marker='^', zorder=5)

elif macd_clean[i] < signal_clean[i] and macd_clean[i-1] >= signal_clean[i-1]:

ax2.scatter(i, macd_clean[i], color='red', s=100, marker='v', zorder=5)

ax2.set_title('MACD Lines', fontsize=14, fontweight='bold')

ax2.set_ylabel('MACD', fontsize=12)

ax2.legend(fontsize=10)

ax2.grid(True, alpha=0.3)

# MACD Histogram

colors = ['green' if h >= 0 else 'red' for h in histogram]

ax3.bar(range(len(histogram)), histogram, color=colors, alpha=0.7, width=0.8)

ax3.axhline(y=0, color='gray', linestyle='-', alpha=0.5)

ax3.set_title('MACD Histogram', fontsize=14, fontweight='bold')

ax3.set_xlabel('Days', fontsize=12)

ax3.set_ylabel('Histogram', fontsize=12)

ax3.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

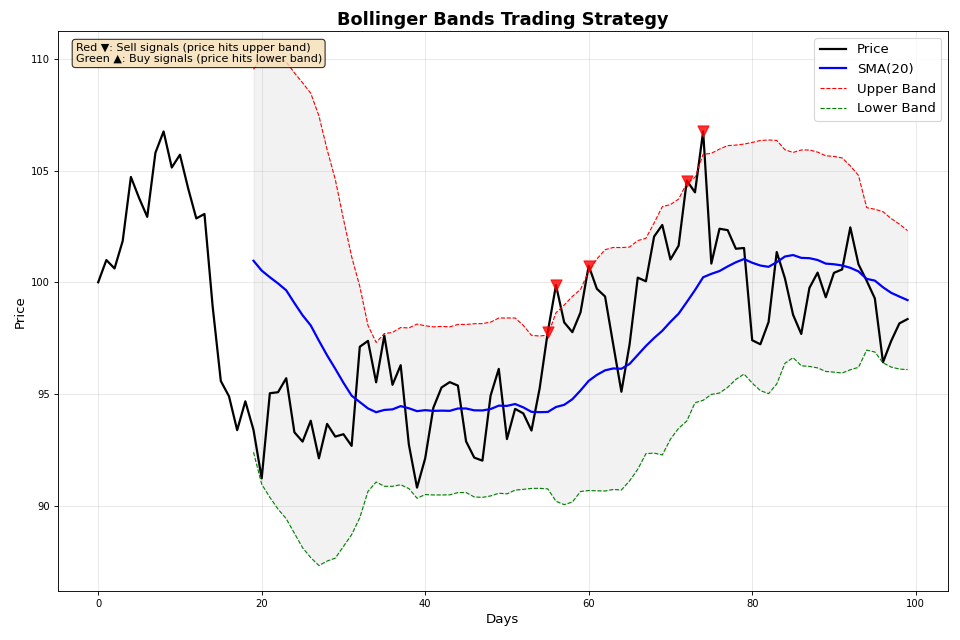

Bollinger Bands Strategy

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.indicators import TechnicalIndicators

# Generate mean-reverting price data

np.random.seed(42)

mean_price = 100

prices = [mean_price]

for i in range(99):

reversion = 0.1 * (mean_price - prices[-1])

noise = np.random.normal(0, 2)

new_price = prices[-1] + reversion + noise

prices.append(new_price)

prices = np.array(prices)

# Calculate Bollinger Bands

upper, middle, lower = TechnicalIndicators.bollinger_bands(prices, 20, 2)

# Create the plot

fig, ax = plt.subplots(figsize=(12, 8))

# Plot Bollinger Bands

ax.plot(prices, color='black', linewidth=2, label='Price')

ax.plot(middle, color='blue', linewidth=2, label='SMA(20)')

ax.plot(upper, color='red', linewidth=1, linestyle='--', label='Upper Band')

ax.plot(lower, color='green', linewidth=1, linestyle='--', label='Lower Band')

# Fill between bands

ax.fill_between(range(len(prices)), upper, lower, alpha=0.1, color='gray')

# Mark trading signals

for i in range(20, len(prices)):

if not np.isnan(upper[i]) and not np.isnan(lower[i]):

if prices[i] >= upper[i]:

ax.scatter(i, prices[i], color='red', s=100, marker='v', zorder=5, alpha=0.8)

elif prices[i] <= lower[i]:

ax.scatter(i, prices[i], color='green', s=100, marker='^', zorder=5, alpha=0.8)

# Calculate band width for squeeze detection

band_width = (upper - lower) / middle

squeeze_threshold = np.nanpercentile(band_width, 20) # Bottom 20%

ax.set_title('Bollinger Bands Trading Strategy', fontsize=16, fontweight='bold')

ax.set_xlabel('Days', fontsize=12)

ax.set_ylabel('Price', fontsize=12)

ax.legend(fontsize=12)

ax.grid(True, alpha=0.3)

# Add annotations

ax.text(0.02, 0.98, f'Red ▼: Sell signals (price hits upper band)\nGreen ▲: Buy signals (price hits lower band)',

transform=ax.transAxes, fontsize=10, verticalalignment='top',

bbox=dict(boxstyle='round', facecolor='wheat', alpha=0.8))

plt.tight_layout()

plt.show()

Portfolio Analytics Visualization

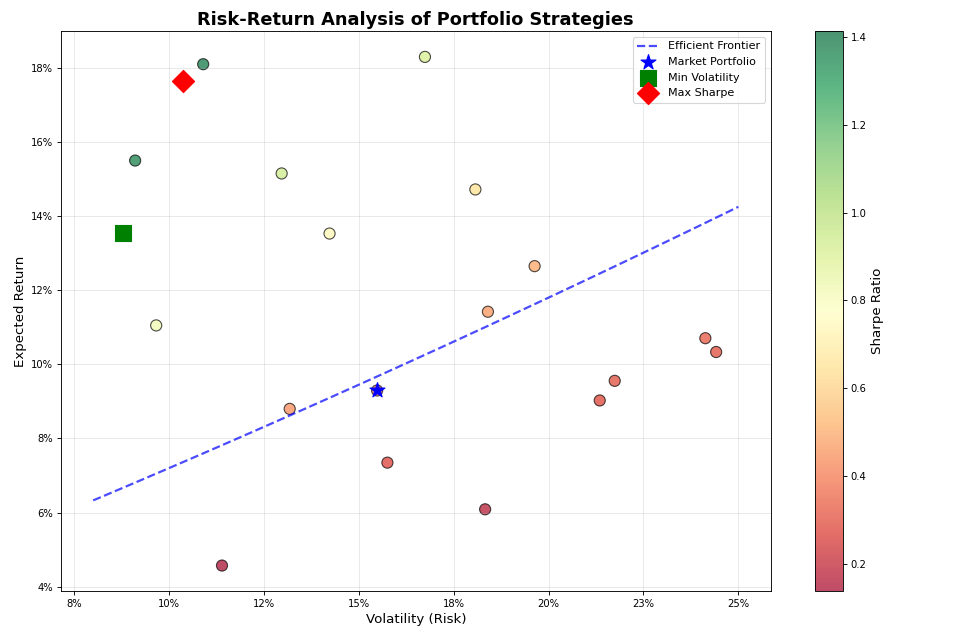

Risk-Return Scatter Plot

import numpy as np

import matplotlib.pyplot as plt

# Simulate multiple portfolio strategies

np.random.seed(42)

n_strategies = 20

# Generate risk-return data for different strategies

returns = np.random.uniform(0.05, 0.20, n_strategies) # 5% to 20% annual returns

volatilities = np.random.uniform(0.08, 0.25, n_strategies) # 8% to 25% volatility

# Add some correlation between risk and return

returns = returns + 0.3 * (volatilities - np.mean(volatilities))

# Calculate Sharpe ratios

risk_free_rate = 0.03

sharpe_ratios = (returns - risk_free_rate) / volatilities

# Create the plot

fig, ax = plt.subplots(figsize=(12, 8))

# Color points by Sharpe ratio

scatter = ax.scatter(volatilities, returns, c=sharpe_ratios, s=100,

cmap='RdYlGn', alpha=0.7, edgecolors='black', linewidth=1)

# Add efficient frontier curve

efficient_vol = np.linspace(0.08, 0.25, 50)

efficient_ret = 0.03 + 0.4 * efficient_vol + 0.2 * efficient_vol**2

ax.plot(efficient_vol, efficient_ret, 'b--', linewidth=2, alpha=0.7, label='Efficient Frontier')

# Mark special portfolios

market_idx = np.argmin(np.abs(volatilities - 0.15)) # Market portfolio

min_vol_idx = np.argmin(volatilities) # Minimum volatility

max_sharpe_idx = np.argmax(sharpe_ratios) # Maximum Sharpe

ax.scatter(volatilities[market_idx], returns[market_idx],

color='blue', s=200, marker='*', label='Market Portfolio', zorder=5)

ax.scatter(volatilities[min_vol_idx], returns[min_vol_idx],

color='green', s=200, marker='s', label='Min Volatility', zorder=5)

ax.scatter(volatilities[max_sharpe_idx], returns[max_sharpe_idx],

color='red', s=200, marker='D', label='Max Sharpe', zorder=5)

# Add colorbar

cbar = plt.colorbar(scatter)

cbar.set_label('Sharpe Ratio', fontsize=12)

# Styling

ax.set_title('Risk-Return Analysis of Portfolio Strategies', fontsize=16, fontweight='bold')

ax.set_xlabel('Volatility (Risk)', fontsize=12)

ax.set_ylabel('Expected Return', fontsize=12)

ax.legend(fontsize=10)

ax.grid(True, alpha=0.3)

# Format axes as percentages

ax.xaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.0%}'))

ax.yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.0%}'))

plt.tight_layout()

plt.show()

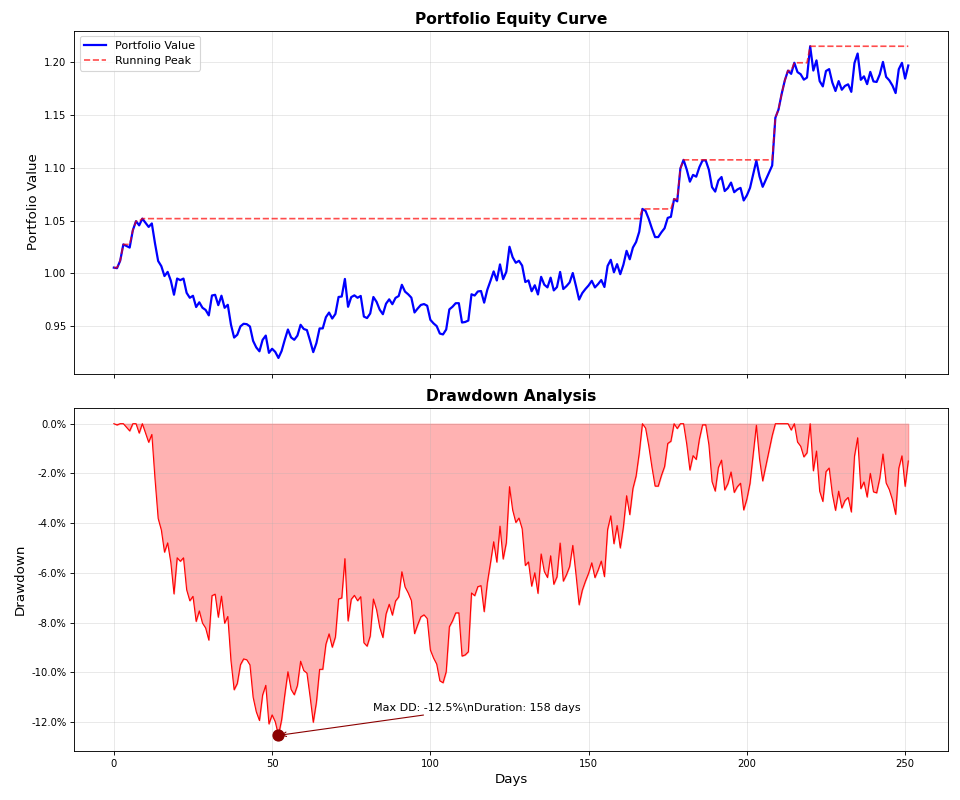

Drawdown Analysis

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.portfolio import AdvancedPortfolioAnalytics

# Simulate portfolio returns with drawdown periods

np.random.seed(42)

# Create realistic return series with volatility clustering

returns = []

vol = 0.15 # Starting volatility

for i in range(252): # One year of daily returns

# GARCH-like volatility

vol = 0.95 * vol + 0.05 * 0.15 + 0.1 * abs(returns[-1] if returns else 0)

ret = np.random.normal(0.0008, vol / np.sqrt(252)) # Daily return

returns.append(ret)

returns = np.array(returns)

equity_curve = np.cumprod(1 + returns)

# Calculate drawdowns

peak = np.maximum.accumulate(equity_curve)

drawdown = (equity_curve - peak) / peak

# Create the plot

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(12, 10), sharex=True)

# Equity curve

ax1.plot(equity_curve, color='blue', linewidth=2, label='Portfolio Value')

ax1.plot(peak, color='red', linestyle='--', alpha=0.7, label='Running Peak')

ax1.set_title('Portfolio Equity Curve', fontsize=14, fontweight='bold')

ax1.set_ylabel('Portfolio Value', fontsize=12)

ax1.legend(fontsize=10)

ax1.grid(True, alpha=0.3)

# Drawdown chart

ax2.fill_between(range(len(drawdown)), drawdown, 0, alpha=0.3, color='red')

ax2.plot(drawdown, color='red', linewidth=1)

ax2.set_title('Drawdown Analysis', fontsize=14, fontweight='bold')

ax2.set_xlabel('Days', fontsize=12)

ax2.set_ylabel('Drawdown', fontsize=12)

ax2.grid(True, alpha=0.3)

# Format y-axis as percentage

ax2.yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.1%}'))

# Add statistics

analytics = AdvancedPortfolioAnalytics(returns)

max_dd, duration, max_dd_idx = analytics.calculate_maximum_drawdown(equity_curve)

# Mark maximum drawdown

ax2.scatter(max_dd_idx, max_dd, color='darkred', s=100, zorder=5)

ax2.annotate(f'Max DD: {max_dd:.1%}\\nDuration: {duration} days',

xy=(max_dd_idx, max_dd), xytext=(max_dd_idx + 30, max_dd + 0.01),

arrowprops=dict(arrowstyle='->', color='darkred'),

fontsize=10, ha='left')

plt.tight_layout()

plt.show()

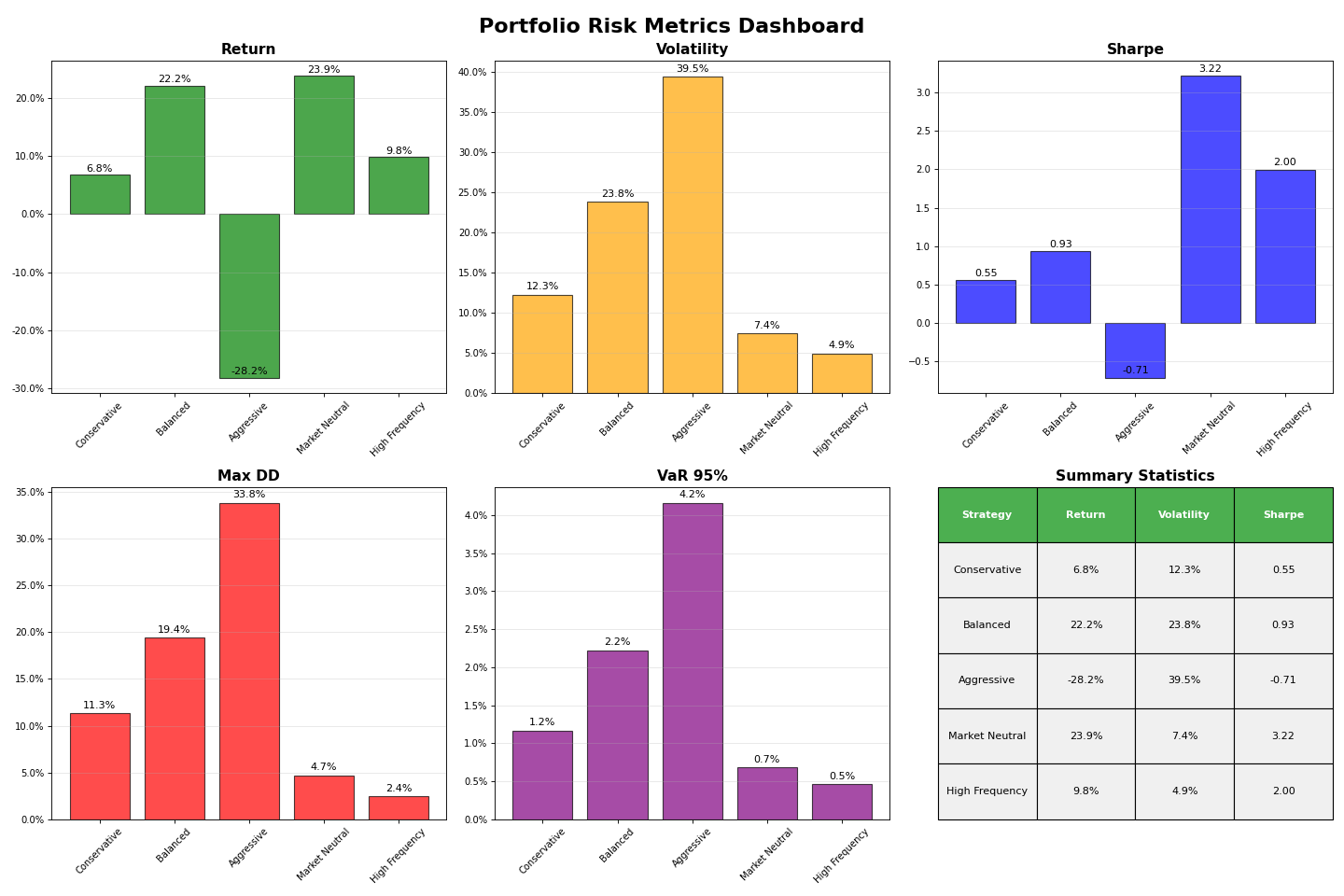

Risk Metrics Dashboard

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.append('/workspaces/Portfolio-lib/portfolio-lib-package')

from portfolio_lib.portfolio import AdvancedPortfolioAnalytics

# Generate sample returns for multiple strategies

np.random.seed(42)

strategies = ['Conservative', 'Balanced', 'Aggressive', 'Market Neutral', 'High Frequency']

# Different return profiles

strategy_params = {

'Conservative': (0.0003, 0.008), # Low return, low vol

'Balanced': (0.0005, 0.015), # Medium return, medium vol

'Aggressive': (0.0008, 0.025), # High return, high vol

'Market Neutral': (0.0002, 0.005), # Very low return and vol

'High Frequency': (0.0001, 0.003) # Very low vol, minimal return

}

metrics_data = {}

for strategy, (daily_ret, daily_vol) in strategy_params.items():

returns = np.random.normal(daily_ret, daily_vol, 252)

equity_curve = np.cumprod(1 + returns)

analytics = AdvancedPortfolioAnalytics(returns)

# Calculate key metrics

annual_return = np.mean(returns) * 252

annual_vol = np.std(returns) * np.sqrt(252)

sharpe = annual_return / annual_vol if annual_vol > 0 else 0

max_dd, _, _ = analytics.calculate_maximum_drawdown(equity_curve)

var_95 = analytics.calculate_var(0.05)

metrics_data[strategy] = {

'Return': annual_return,

'Volatility': annual_vol,

'Sharpe': sharpe,

'Max DD': abs(max_dd),

'VaR 95%': abs(var_95)

}

# Create dashboard

fig, axes = plt.subplots(2, 3, figsize=(18, 12))

fig.suptitle('Portfolio Risk Metrics Dashboard', fontsize=20, fontweight='bold')

metrics = ['Return', 'Volatility', 'Sharpe', 'Max DD', 'VaR 95%']

colors = ['green', 'orange', 'blue', 'red', 'purple']

for i, metric in enumerate(metrics):

if i < 5: # We have 6 subplots, use 5

ax = axes[i//3, i%3]

values = [metrics_data[strategy][metric] for strategy in strategies]

bars = ax.bar(strategies, values, color=colors[i], alpha=0.7, edgecolor='black')

ax.set_title(f'{metric}', fontsize=14, fontweight='bold')

ax.tick_params(axis='x', rotation=45)

ax.grid(True, alpha=0.3, axis='y')

# Format y-axis based on metric type

if metric in ['Return', 'Volatility', 'Max DD', 'VaR 95%']:

ax.yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'{x:.1%}'))

# Add value labels on bars

for bar, value in zip(bars, values):

height = bar.get_height()

if metric in ['Return', 'Volatility', 'Max DD', 'VaR 95%']:

label = f'{value:.1%}'

else:

label = f'{value:.2f}'

ax.text(bar.get_x() + bar.get_width()/2., height + max(values)*0.01,

label, ha='center', va='bottom', fontsize=10)

# Use the last subplot for a summary table

ax = axes[1, 2]

ax.axis('off')

# Create table data

table_data = []

for strategy in strategies:

row = [strategy]

for metric in ['Return', 'Volatility', 'Sharpe']:

value = metrics_data[strategy][metric]

if metric in ['Return', 'Volatility']:

row.append(f'{value:.1%}')

else:

row.append(f'{value:.2f}')

table_data.append(row)

# Create table

table = ax.table(cellText=table_data,

colLabels=['Strategy', 'Return', 'Volatility', 'Sharpe'],

cellLoc='center',

loc='center',

bbox=[0, 0, 1, 1])

table.auto_set_font_size(False)

table.set_fontsize(10)

table.scale(1, 2)

# Style the table

for i in range(len(strategies) + 1):

for j in range(4):

cell = table[(i, j)]

if i == 0: # Header

cell.set_facecolor('#4CAF50')

cell.set_text_props(weight='bold', color='white')

else:

cell.set_facecolor('#f0f0f0')

ax.set_title('Summary Statistics', fontsize=14, fontweight='bold')

plt.tight_layout()

plt.show()

Mathematical Formulas Reference

Key Technical Indicator Formulas

Indicator |

Formula |

Description |

|---|---|---|

Simple Moving Average |

\(SMA_t = \frac{1}{n} \sum_{i=0}^{n-1} P_{t-i}\) |

Average of last n prices |

Exponential Moving Average |

\(EMA_t = \alpha P_t + (1-\alpha) EMA_{t-1}\) where \(\alpha = \frac{2}{n+1}\) |

Weighted average giving more weight to recent prices |

Relative Strength Index |

\(RSI = 100 - \frac{100}{1 + RS}\) where \(RS = \frac{Avg Gain}{Avg Loss}\) |

Momentum oscillator (0-100) |

MACD |

\(MACD = EMA_{fast} - EMA_{slow}\) |

Trend-following momentum indicator |

Bollinger Bands |

\(Upper = SMA + (k \times \sigma)\), \(Lower = SMA - (k \times \sigma)\) |

Volatility bands around moving average |

Stochastic %K |

\(\%K = 100 \times \frac{C - L_n}{H_n - L_n}\) |

Position within recent price range |

Williams %R |

\(\%R = -100 \times \frac{H_n - C}{H_n - L_n}\) |

Inverted stochastic oscillator |

Average True Range |

\(ATR = SMA(TR)\) where \(TR = \max(H-L, |H-C_{prev}|, |L-C_{prev}|)\) |

Measure of volatility |

Portfolio Risk Metrics Formulas

Metric |

Formula |

Description |

|---|---|---|

Value at Risk (VaR) |

\(VaR_\alpha = -\inf\{x : P(X \leq x) \geq \alpha\}\) |

Maximum loss at confidence level α |

Conditional VaR (CVaR) |

\(CVaR_\alpha = E[X | X \leq VaR_\alpha]\) |

Expected loss beyond VaR |

Maximum Drawdown |

\(MDD = \max_{t \in [0,T]} \left[ \frac{Peak_t - Valley_t}{Peak_t} \right]\) |

Largest peak-to-trough decline |

Sharpe Ratio |

\(SR = \frac{E[R_p] - R_f}{\sigma_p}\) |

Risk-adjusted return measure |

Beta |

\(\beta = \frac{Cov(R_p, R_m)}{Var(R_m)}\) |

Systematic risk measure |

Alpha |

\(\alpha = E[R_p] - (R_f + \beta(E[R_m] - R_f))\) |

Risk-adjusted excess return |

Tracking Error |

\(TE = \sigma(R_p - R_b)\) |

Volatility of excess returns |

Information Ratio |

\(IR = \frac{E[R_p - R_b]}{TE}\) |

Risk-adjusted active return |

Position Sizing Formulas

Method |

Formula |

Description |

|---|---|---|

Kelly Criterion |

\(f^* = \frac{bp - q}{b}\) where b=odds, p=win prob, q=loss prob |

Optimal fraction for maximum growth |

Fixed Fractional |

\(Position = \frac{Account \times Risk\%}{Stop Loss\%}\) |

Fixed percentage risk per trade |

Volatility Targeting |

\(Leverage = \frac{Target Vol}{Asset Vol}\) |

Scale position based on volatility |

Risk Parity |

\(w_i \times (Cov \times w)_i = \frac{\sigma_p}{n}\) for all i |

Equal risk contribution from each asset |

Performance Attribution Formulas

Component |

Formula |

Description |

|---|---|---|

Allocation Effect |

\((w_p - w_b) \times r_b\) |

Impact of weight differences |

Selection Effect |

\(w_b \times (r_p - r_b)\) |

Impact of security selection |

Interaction Effect |

\((w_p - w_b) \times (r_p - r_b)\) |

Combined allocation and selection |

Total Attribution |

\(Allocation + Selection + Interaction\) |

Sum of all attribution effects |

where: - \(w_p, w_b\) = Portfolio and benchmark weights - \(r_p, r_b\) = Portfolio and benchmark returns - \(\sigma\) = Standard deviation - \(n\) = Number of periods or assets - \(Cov\) = Covariance matrix