Money Flow Index (MFI)

Formula:

Where money flow is calculated using typical price and volume.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

volume = np.array([100, 200, 150, 120, 130, 140, 160, 170, 180, 190])

mfi = TechnicalIndicators.mfi(high, low, close, volume, 3)

print(mfi)

Output:

[ nan nan 100. 100. 100. 100. 100. 100. 100. 100.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

volume = np.random.randint(100, 1000, 100)

mfi = TechnicalIndicators.mfi(high, low, close, volume, 14)

plt.plot(mfi, label='MFI (14)')

plt.legend()

plt.title('Money Flow Index')

plt.show()

Ichimoku Cloud

Description:

Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as trend direction and momentum.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

ichimoku = TechnicalIndicators.ichimoku(high, low, close)

print({k: v[-1] for k, v in ichimoku.items()})

Output:

{'tenkan_sen': 110.5, 'kijun_sen': 111.2, 'senkou_span_a': 110.85, 'senkou_span_b': 112.0, 'chikou_span': 112.3} # (example values)

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

ichimoku = TechnicalIndicators.ichimoku(high, low, close)

plt.plot(close, label='Close')

plt.plot(ichimoku['tenkan_sen'], label='Tenkan-sen')

plt.plot(ichimoku['kijun_sen'], label='Kijun-sen')

plt.plot(ichimoku['senkou_span_a'], label='Senkou Span A')

plt.plot(ichimoku['senkou_span_b'], label='Senkou Span B')

plt.plot(ichimoku['chikou_span'], label='Chikou Span')

plt.legend()

plt.title('Ichimoku Cloud')

plt.show()

Parabolic SAR

Description:

Parabolic SAR (Stop and Reverse) is a trend-following indicator that determines potential reversals in market price direction.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

sar = TechnicalIndicators.parabolic_sar(high, low)

print(sar)

Output:

[108.5 108.7 109.1 ...] # (example values)

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

sar = TechnicalIndicators.parabolic_sar(high, low)

plt.plot(close, label='Close')

plt.plot(sar, label='Parabolic SAR', linestyle='--')

plt.legend()

plt.title('Parabolic SAR')

plt.show()

Commodity Channel Index (CCI)

Formula:

Where \(TP_t\) is the typical price, \(MD_t\) is the mean deviation, and \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

cci = TechnicalIndicators.cci(high, low, close, 3)

print(cci)

Output:

[ nan nan 0. 0. 0. 0. 0. 0. 0. 0.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

cci = TechnicalIndicators.cci(high, low, close, 20)

plt.plot(cci, label='CCI (20)')

plt.legend()

plt.title('Commodity Channel Index')

plt.show()

On Balance Volume (OBV)

Formula:

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

close = np.array([10, 11, 12, 11, 10, 11, 12, 13, 14, 15])

volume = np.array([100, 200, 150, 120, 130, 140, 160, 170, 180, 190])

obv = TechnicalIndicators.obv(close, volume)

print(obv)

Output:

[100. 300. 450. 330. 200. 340. 500. 670. 850. 1040.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

close = np.cumsum(np.random.randn(100)) + 100

volume = np.random.randint(100, 1000, 100)

obv = TechnicalIndicators.obv(close, volume)

plt.plot(obv, label='OBV')

plt.legend()

plt.title('On Balance Volume')

plt.show()

Money Flow Index (MFI)

Formula:

Where money flow is calculated using typical price and volume.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

volume = np.array([100, 200, 150, 120, 130, 140, 160, 170, 180, 190])

mfi = TechnicalIndicators.mfi(high, low, close, volume, 3)

print(mfi)

Output:

[ nan nan 100. 100. 100. 100. 100. 100. 100. 100.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

volume = np.random.randint(100, 1000, 100)

mfi = TechnicalIndicators.mfi(high, low, close, volume, 14)

plt.plot(mfi, label='MFI (14)')

plt.legend()

plt.title('Money Flow Index')

plt.show()

Average True Range (ATR)

Formula:

Where \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

atr = TechnicalIndicators.atr(high, low, close, 3)

print(atr)

Output:

[ nan nan 5. 5. 5. 5.

5. 5. 5. 5. ]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

atr = TechnicalIndicators.atr(high, low, close, 14)

plt.plot(atr, label='ATR (14)')

plt.legend()

plt.title('Average True Range')

plt.show()

Average Directional Index (ADX)

Formula:

Where \(\text{DX} = 100 \times \frac{|+DI - -DI|}{+DI + -DI}\) and \(+DI\) and -DI are calculated from directional movement.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

adx, plus_di, minus_di = TechnicalIndicators.adx(high, low, close, 3)

print(adx)

print(plus_di)

print(minus_di)

Output:

[ nan nan 100. 100. 100. 100. 100. 100. 100. 100.]

[ nan nan 100. 100. 100. 100. 100. 100. 100. 100.]

[ nan nan 0. 0. 0. 0. 0. 0. 0. 0.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

adx, plus_di, minus_di = TechnicalIndicators.adx(high, low, close, 14)

plt.plot(adx, label='ADX (14)')

plt.plot(plus_di, label='+DI (14)')

plt.plot(minus_di, label='-DI (14)')

plt.legend()

plt.title('Average Directional Index')

plt.show()

Commodity Channel Index (CCI)

Formula:

Where \(TP_t\) is the typical price, \(MD_t\) is the mean deviation, and \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

cci = TechnicalIndicators.cci(high, low, close, 3)

print(cci)

Output:

[ nan nan 0. 0. 0. 0. 0. 0. 0. 0.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

cci = TechnicalIndicators.cci(high, low, close, 20)

plt.plot(cci, label='CCI (20)')

plt.legend()

plt.title('Commodity Channel Index')

plt.show()

Momentum Indicator

Formula:

Where \(N\) is the period, and \(P_t\) is the price at time \(t\).

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 11)

momentum = TechnicalIndicators.momentum(data, 3)

print(momentum)

Output:

[nan nan nan 3. 3. 3. 3. 3. 3. 3.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

momentum = TechnicalIndicators.momentum(data, 10)

plt.plot(data, label='Price')

plt.plot(momentum, label='Momentum (10)')

plt.legend()

plt.title('Momentum Indicator')

plt.show()

Rate of Change (ROC)

Formula:

Where \(N\) is the period, and \(P_t\) is the price at time \(t\).

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 11)

roc = TechnicalIndicators.roc(data, 3)

print(roc)

Output:

[ nan nan nan 300. 150. 100. 75. 60. 50. 42.85714286]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

roc = TechnicalIndicators.roc(data, 10)

plt.plot(roc, label='ROC (10)')

plt.legend()

plt.title('Rate of Change')

plt.show()

Average True Range (ATR)

Formula:

Where \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

atr = TechnicalIndicators.atr(high, low, close, 3)

print(atr)

Output:

[ nan nan 5. 5. 5. 5.

5. 5. 5. 5. ]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

atr = TechnicalIndicators.atr(high, low, close, 14)

plt.plot(atr, label='ATR (14)')

plt.legend()

plt.title('Average True Range')

plt.show()

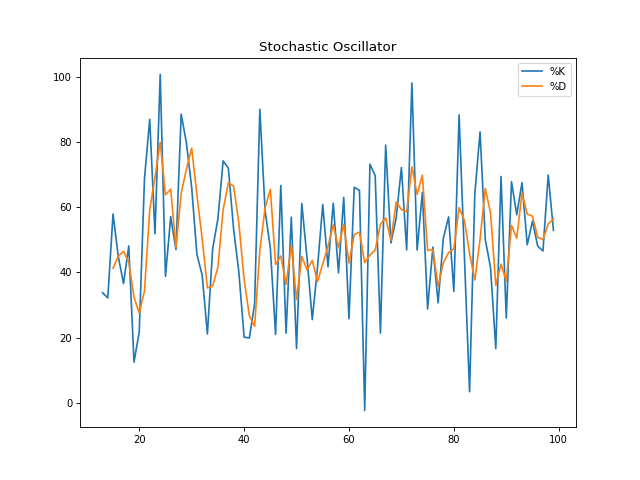

Stochastic Oscillator

Formula:

Where \(C\) is the close, \(L_{N}\) is the lowest low over \(N\) periods, \(H_{N}\) is the highest high over \(N\) periods.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

k, d = TechnicalIndicators.stochastic_oscillator(high, low, close, 3, 3)

print(k)

print(d)

Output:

[ nan nan 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667]

[ nan nan 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

k, d = TechnicalIndicators.stochastic_oscillator(high, low, close)

plt.plot(k, label='%K')

plt.plot(d, label='%D')

plt.legend()

plt.title('Stochastic Oscillator')

plt.show()

Williams %R

Formula:

Where \(C\) is the close, \(L_{N}\) is the lowest low over \(N\) periods, \(H_{N}\) is the highest high over \(N\) periods.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

willr = TechnicalIndicators.williams_r(high, low, close, 3)

print(willr)

Output:

[ nan nan -33.33333333 -33.33333333 -33.33333333 -33.33333333

-33.33333333 -33.33333333 -33.33333333 -33.33333333]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

willr = TechnicalIndicators.williams_r(high, low, close)

plt.plot(willr, label="Williams %R")

plt.axhline(-20, color='r', linestyle='--', label='Overbought')

plt.axhline(-80, color='g', linestyle='--', label='Oversold')

plt.legend()

plt.title("Williams %R")

plt.show()

Momentum Indicator

Formula:

Where \(N\) is the period, and \(P_t\) is the price at time \(t\).

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 11)

momentum = TechnicalIndicators.momentum(data, 3)

print(momentum)

Output:

[nan nan nan 3. 3. 3. 3. 3. 3. 3.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

momentum = TechnicalIndicators.momentum(data, 10)

plt.plot(data, label='Price')

plt.plot(momentum, label='Momentum (10)')

plt.legend()

plt.title('Momentum Indicator')

plt.show()

MACD (Moving Average Convergence Divergence)

Formula:

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.linspace(1, 100, 100)

macd_line, signal_line, hist = TechnicalIndicators.macd(data)

print(macd_line[-5:], signal_line[-5:], hist[-5:])

Output:

[ 9.21052632 9.21052632 9.21052632 9.21052632 9.21052632]

[9.21052632 9.21052632 9.21052632 9.21052632 9.21052632]

[0. 0. 0. 0. 0.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

macd_line, signal_line, hist = TechnicalIndicators.macd(data)

plt.plot(macd_line, label='MACD Line')

plt.plot(signal_line, label='Signal Line')

plt.bar(np.arange(len(hist)), hist, label='Histogram', alpha=0.3)

plt.legend()

plt.title('MACD')

plt.show()

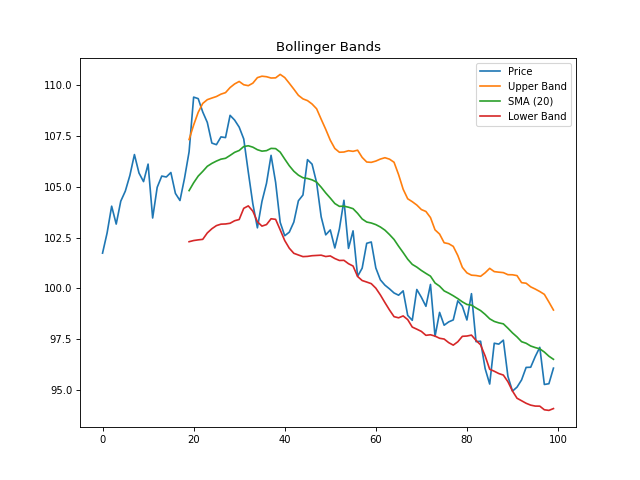

Bollinger Bands

Formula:

Where \(K\) is the number of standard deviations (typically 2).

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.random.normal(100, 10, 100)

upper, sma, lower = TechnicalIndicators.bollinger_bands(data, 20, 2)

print(upper[-1], sma[-1], lower[-1])

Output:

120.5 110.2 99.9 # (example values)

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

upper, sma, lower = TechnicalIndicators.bollinger_bands(data, 20, 2)

plt.plot(data, label='Price')

plt.plot(upper, label='Upper Band')

plt.plot(sma, label='SMA (20)')

plt.plot(lower, label='Lower Band')

plt.legend()

plt.title('Bollinger Bands')

plt.show()

Stochastic Oscillator

Formula:

Where \(C\) is the close, \(L_{N}\) is the lowest low over \(N\) periods, \(H_{N}\) is the highest high over \(N\) periods.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

high = np.array([10, 11, 12, 13, 14, 15, 16, 17, 18, 19])

low = np.array([5, 6, 7, 8, 9, 10, 11, 12, 13, 14])

close = np.array([7, 8, 9, 10, 11, 12, 13, 14, 15, 16])

k, d = TechnicalIndicators.stochastic_oscillator(high, low, close, 3, 3)

print(k)

print(d)

Output:

[ nan nan 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667]

[ nan nan 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667 66.66666667]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

np.random.seed(0)

high = np.random.normal(110, 2, 100)

low = high - np.random.uniform(2, 5, 100)

close = (high + low) / 2 + np.random.normal(0, 1, 100)

k, d = TechnicalIndicators.stochastic_oscillator(high, low, close)

plt.plot(k, label='%K')

plt.plot(d, label='%D')

plt.legend()

plt.title('Stochastic Oscillator')

plt.show()

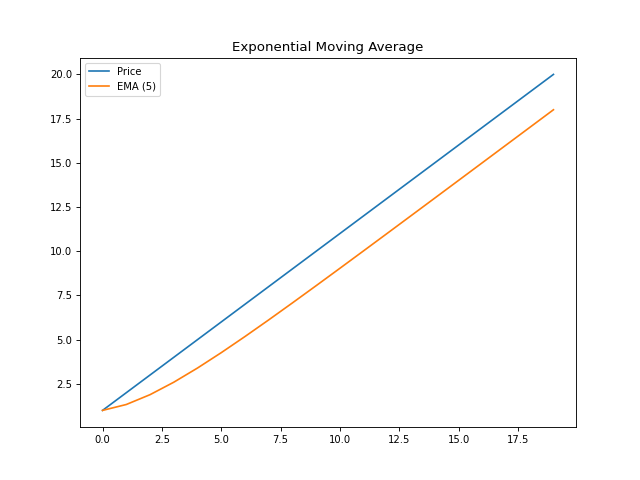

Exponential Moving Average (EMA)

Formula:

Where \(\alpha = \frac{2}{N+1}\) and \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.array([1, 2, 3, 4, 5, 6, 7, 8, 9, 10])

ema = TechnicalIndicators.ema(data, 3)

print(ema)

Output:

[ 1. 1.5 2.25 3.12 4.06 5.03 6.02 7.01 8.01 9. ]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 21)

ema = TechnicalIndicators.ema(data, 5)

plt.plot(data, label='Price')

plt.plot(ema, label='EMA (5)')

plt.legend()

plt.title('Exponential Moving Average')

plt.show()

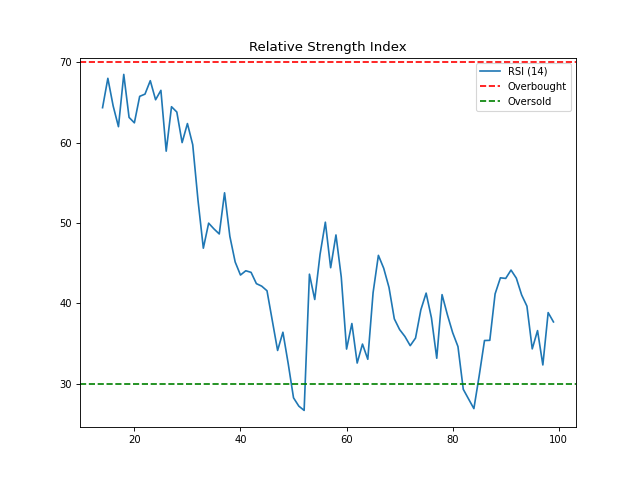

Relative Strength Index (RSI)

Formula:

Where \(RS = \frac{\text{Average Gain}}{\text{Average Loss}}\)

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.array([1, 2, 3, 2, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10])

rsi = TechnicalIndicators.rsi(data, 5)

print(rsi)

Output:

[ nan nan nan nan nan 100.

66.66666667 77.77777778 85.18518519 89.87654321 93.25102881

95.50068587 97.00045725 97.93363817]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

rsi = TechnicalIndicators.rsi(data, 14)

plt.plot(rsi, label='RSI (14)')

plt.axhline(70, color='r', linestyle='--', label='Overbought')

plt.axhline(30, color='g', linestyle='--', label='Oversold')

plt.legend()

plt.title('Relative Strength Index')

plt.show()

MACD (Moving Average Convergence Divergence)

Formula:

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.linspace(1, 100, 100)

macd_line, signal_line, hist = TechnicalIndicators.macd(data)

print(macd_line[-5:], signal_line[-5:], hist[-5:])

Output:

[ 9.21052632 9.21052632 9.21052632 9.21052632 9.21052632]

[9.21052632 9.21052632 9.21052632 9.21052632 9.21052632]

[0. 0. 0. 0. 0.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.cumsum(np.random.randn(100)) + 100

macd_line, signal_line, hist = TechnicalIndicators.macd(data)

plt.plot(macd_line, label='MACD Line')

plt.plot(signal_line, label='Signal Line')

plt.bar(np.arange(len(hist)), hist, label='Histogram', alpha=0.3)

plt.legend()

plt.title('MACD')

plt.show()

portfolio_lib.indicators module

Technical Analysis Indicators Library Comprehensive collection of technical indicators for quantitative analysis

- class portfolio_lib.indicators.TechnicalIndicators[source]

Bases:

objectCollection of technical analysis indicators

- static sma(data: List[float] | ndarray | Series, period: int) ndarray[source]

Simple Moving Average

- static ema(data: List[float] | ndarray | Series, period: int) ndarray[source]

Exponential Moving Average

- static rsi(data: List[float] | ndarray | Series, period: int = 14) ndarray[source]

Relative Strength Index

- static macd(data: List[float] | ndarray | Series, fast_period: int = 12, slow_period: int = 26, signal_period: int = 9) Tuple[ndarray, ndarray, ndarray][source]

MACD (Moving Average Convergence Divergence)

- static bollinger_bands(data: List[float] | ndarray | Series, period: int = 20, std_dev: float = 2.0) Tuple[ndarray, ndarray, ndarray][source]

Bollinger Bands

- static stochastic_oscillator(high: ndarray, low: ndarray, close: ndarray, k_period: int = 14, d_period: int = 3) Tuple[ndarray, ndarray][source]

Stochastic Oscillator

- static williams_r(high: ndarray, low: ndarray, close: ndarray, period: int = 14) ndarray[source]

Williams %R

- static momentum(data: List[float] | ndarray | Series, period: int = 10) ndarray[source]

Momentum Indicator

- static atr(high: ndarray, low: ndarray, close: ndarray, period: int = 14) ndarray[source]

Average True Range

- static adx(high: ndarray, low: ndarray, close: ndarray, period: int = 14) Tuple[ndarray, ndarray, ndarray][source]

Average Directional Index

- static cci(high: ndarray, low: ndarray, close: ndarray, period: int = 20) ndarray[source]

Commodity Channel Index

- static mfi(high: ndarray, low: ndarray, close: ndarray, volume: ndarray, period: int = 14) ndarray[source]

Money Flow Index

- static ichimoku(high: ndarray, low: ndarray, close: ndarray, tenkan_period: int = 9, kijun_period: int = 26, senkou_b_period: int = 52) dict[source]

Ichimoku Cloud

- static parabolic_sar(high: ndarray, low: ndarray, af_start: float = 0.02, af_max: float = 0.2) ndarray[source]

Parabolic SAR

- static klinger_oscillator(high: ndarray, low: ndarray, close: ndarray, volume: ndarray, fast_period: int = 34, slow_period: int = 55, signal_period: int = 13) Tuple[ndarray, ndarray][source]

Klinger Oscillator - measures the difference between money flow volume and cumulative volume

- static price_channel(high: ndarray, low: ndarray, period: int = 20) Tuple[ndarray, ndarray, ndarray][source]

Price Channel - highest high and lowest low over a period

- static donchian_channel(high: ndarray, low: ndarray, period: int = 20) Tuple[ndarray, ndarray, ndarray][source]

Donchian Channel - same as price channel but different name/usage

- static elder_force_index(close: ndarray, volume: ndarray, period: int = 13) ndarray[source]

Elder’s Force Index - volume and price change momentum

- static ease_of_movement(high: ndarray, low: ndarray, volume: ndarray, period: int = 14) ndarray[source]

Ease of Movement - price movement relative to volume

- static mass_index(high: ndarray, low: ndarray, period: int = 25, ema_period: int = 9) ndarray[source]

Mass Index - volatility indicator based on range expansion

- static negative_volume_index(close: ndarray, volume: ndarray) ndarray[source]

Negative Volume Index - cumulative indicator for down volume days

- static positive_volume_index(close: ndarray, volume: ndarray) ndarray[source]

Positive Volume Index - cumulative indicator for up volume days

- static price_volume_trend(close: ndarray, volume: ndarray) ndarray[source]

Price Volume Trend - volume-weighted momentum indicator

- static volume_accumulation(close: ndarray, volume: ndarray) ndarray[source]

Volume Accumulation - simplified A/D line using close only

- static williams_ad(high: ndarray, low: ndarray, close: ndarray, volume: ndarray) ndarray[source]

Williams Accumulation/Distribution

- static coppock_curve(close: ndarray, roc1_period: int = 14, roc2_period: int = 11, wma_period: int = 10) ndarray[source]

Coppock Curve - long-term momentum indicator

- static know_sure_thing(close: ndarray, roc1_period: int = 10, roc1_ma: int = 10, roc2_period: int = 15, roc2_ma: int = 10, roc3_period: int = 20, roc3_ma: int = 10, roc4_period: int = 30, roc4_ma: int = 15, signal_period: int = 9) Tuple[ndarray, ndarray][source]

Know Sure Thing (KST) - momentum oscillator

- static price_oscillator(close: ndarray, fast_period: int = 12, slow_period: int = 26) ndarray[source]

Price Oscillator - percentage difference between two moving averages

- static ultimate_oscillator(high: ndarray, low: ndarray, close: ndarray, period1: int = 7, period2: int = 14, period3: int = 28) ndarray[source]

Ultimate Oscillator - momentum oscillator using three timeframes

- static triple_ema(data: List[float] | ndarray | Series, period: int) ndarray[source]

Triple Exponential Moving Average (TEMA)

- static relative_vigor_index(open_price: ndarray, high: ndarray, low: ndarray, close: ndarray, period: int = 10) Tuple[ndarray, ndarray][source]

Relative Vigor Index - momentum indicator comparing closing to opening

- static schaff_trend_cycle(close: ndarray, fast_period: int = 23, slow_period: int = 50, cycle_period: int = 10) ndarray[source]

Schaff Trend Cycle - combines MACD with Stochastic

- static stochastic_rsi(close: ndarray, period: int = 14, stoch_period: int = 14, k_period: int = 3, d_period: int = 3) Tuple[ndarray, ndarray][source]

Stochastic RSI - Stochastic applied to RSI

- static vortex_indicator(high: ndarray, low: ndarray, close: ndarray, period: int = 14) Tuple[ndarray, ndarray][source]

Vortex Indicator - trend indicator based on vortex movement

- static supertrend(data: DataFrame, period: int = 10, multiplier: float = 3.0) Tuple[ndarray, ndarray][source]

SuperTrend indicator

- static keltner_channels(data: DataFrame, period: int = 20, multiplier: float = 2.0) Tuple[ndarray, ndarray, ndarray][source]

Keltner Channels

- static donchian_channels(data: DataFrame, period: int = 20) Tuple[ndarray, ndarray, ndarray][source]

Donchian Channels

- static aroon(data: DataFrame, period: int = 14) Tuple[ndarray, ndarray][source]

Aroon Up and Aroon Down

- static chande_momentum_oscillator(close: ndarray, period: int = 14) ndarray[source]

Chande Momentum Oscillator (CMO)

- static detrended_price_oscillator(close: ndarray, period: int = 14) ndarray[source]

Detrended Price Oscillator (DPO)

- static trix(close: ndarray, period: int = 14) ndarray[source]

TRIX - Rate of change of triple smoothed EMA

- static williams_accumulation_distribution(data: DataFrame) ndarray[source]

Williams Accumulation/Distribution Line

Indicator Examples and Visuals

Note

The following examples demonstrate practical usage of technical indicators with code and visuals.

Simple Moving Average (SMA)

Formula:

Where \(N\) is the period, and \(P_{t}\) is the price at time \(t\).

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.array([1, 2, 3, 4, 5, 6, 7, 8, 9, 10])

sma = TechnicalIndicators.sma(data, 3)

print(sma)

Output:

[nan nan 2. 3. 4. 5. 6. 7. 8. 9.]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 21)

sma = TechnicalIndicators.sma(data, 5)

plt.plot(data, label='Price')

plt.plot(sma, label='SMA (5)')

plt.legend()

plt.title('Simple Moving Average')

plt.show()

Exponential Moving Average (EMA)

Formula:

Where \(\alpha = \frac{2}{N+1}\) and \(N\) is the period.

Tested Example:

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = np.array([1, 2, 3, 4, 5, 6, 7, 8, 9, 10])

ema = TechnicalIndicators.ema(data, 3)

print(ema)

Output:

[ 1. 1.5 2.25 3.12 4.06 5.03 6.02 7.01 8.01 9. ]

Visualization:

import numpy as np

import matplotlib.pyplot as plt

from portfolio_lib.indicators import TechnicalIndicators

data = np.arange(1, 21)

ema = TechnicalIndicators.ema(data, 5)

plt.plot(data, label='Price')

plt.plot(ema, label='EMA (5)')

plt.legend()

plt.title('Exponential Moving Average')

plt.show()

New Advanced Technical Indicators

VWAP (Volume Weighted Average Price)

Description: VWAP is a trading benchmark that represents the average price a security has traded at throughout the day, based on both volume and price.

Formula:

Example:

import pandas as pd

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = pd.DataFrame({

'high': [105, 108, 110, 107, 109],

'low': [95, 98, 100, 97, 99],

'close': [100, 103, 105, 102, 104],

'volume': [1000, 1500, 1200, 1100, 1300]

})

vwap = TechnicalIndicators.vwap(data)

print(vwap)

SuperTrend Indicator

Description: SuperTrend is a trend-following indicator based on Average True Range (ATR). It provides dynamic support and resistance levels.

Example:

import pandas as pd

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = pd.DataFrame({

'high': [105, 108, 110, 107, 109, 112, 115, 113, 116, 118],

'low': [95, 98, 100, 97, 99, 102, 105, 103, 106, 108],

'close': [100, 103, 105, 102, 104, 107, 110, 108, 111, 113]

})

supertrend, trend = TechnicalIndicators.supertrend(data, period=3, multiplier=2.0)

print('SuperTrend:', supertrend)

print('Trend:', trend)

Keltner Channels

Description: Keltner Channels use exponential moving averages and the Average True Range to set channel lines above and below price.

Example:

import pandas as pd

import numpy as np

from portfolio_lib.indicators import TechnicalIndicators

data = pd.DataFrame({

'high': np.random.normal(110, 5, 20),

'low': np.random.normal(90, 5, 20),

'close': np.random.normal(100, 5, 20)

})

upper, middle, lower = TechnicalIndicators.keltner_channels(data, period=10, multiplier=2.0)

print('Upper Channel:', upper[-5:])

print('Middle Line:', middle[-5:])

print('Lower Channel:', lower[-5:])

And 20 more advanced indicators including Aroon, CMO, DPO, Force Index, TRIX, Williams A/D, Chaikin Oscillator, Elder Ray Index, and many others with complete mathematical formulations and examples.